The Risk-Safety Quadrant of Investing

In a world where individuals and institutions are “required” to invest, minimizing risk and finding safety has become a necessity.

Investors often use Risky and Safe as opposite words when assessing an investment. The two words are antonyms of each other in the English language. However, in the world of finance, they can mean a different set of things.

By defining “Risk” and its adjective “Risky” as a different property than “Safe” and its noun “Safety”, a whole new set of different investment outcomes can be achieved.

Risk

A risky investment is one whose value can go up or drop more often and is greater in magnitude than a less risky one. Risk is two-sided. A risky investment can lose more value than a less risky one, but contrastingly also gain more value as a positive surprise.

High risk implies:

- Possibility of high returns.

- Possibility of deep losses.

On the other hand, low risk implies that the investment will have:

- A straight curve that will fluctuate very little (or not at all).

- A predictable final value.

Quantitatively, Risk is linked to Volatility.

High volatility implies high risk and vice versa.

Risk also has behavioral implications for investors. When the value of an investment fluctuates a lot, people with different personalities react to it in a variety of ways. Risk-averse investors may:

- Have butterflies in the stomach.

- Have panic-stricken reactions when a crash happens.

- Try to completely avoid volatile investments.

Such reactions may be the opposite for risk-seeking individuals, who may take up more risk than required. Risk-seekers may over-expose themselves to a volatile investment that may set them up for a ruinous outcome.

Choosing Risk

A good starting point to choose the right type of risk is the underlying asset class. Some asset classes will be inherently riskier than others. Such assets will move faster than other assets and their movements can be much more amplified.

Volatility is inherently linked to asset classes.

For example, we can say that cryptocurrency as an asset class is much riskier than gold or forex. Crypto-currency moves up (and down) much faster and by many more percentage points in a day (or week) than either gold or forex pairs (all of which are denominated in US$ globally).

Similarly, equity can be considered a more risky asset than corporate debt. Even though both equity and debt may be issued by the same company, the value of equity will fluctuate more often than not.

Taming Risk

A practical and easy way to tame risk is position-sizing. Position-sizing means setting rules to limit a portfolio’s exposure to a certain type or category of investments. This allows an investor to take a measured exposure to the volatility offered by an asset class.

Professional investors take “calculated risks” by dividing their portfolios into smaller chunks. They then expose only a few of these chunks to risky opportunities. Position-sizing can be done within the asset class itself and in many more ways.

Position-sizing is the tool to tame risk by limiting exposure to it.

While high-risk (a.k.a. risky) or low-risk determines what the final value can look like, it does not “guarantee” access to the investment. That is a function of Safety.

Safety

Safety means that access to the investment is guaranteed by an authority. This implies that irrespective of the investment value, there will always be a mechanism available to the investors to ensure the continuity of the market for the investment.

Fundamentally, Safety is linked to the structure of the investment.

Unlike risk, it has nothing to do with volatility. Safety is guaranteed by the laws of a country through its regulators or central banks or any other authority. For example, the stock exchange is a structure guaranteed by the government to operate and regulated by the securities board/ commission.

Identifying Unsafe

An unsafe investment is one where you can completely lose access to your money (no matter the value). This can happen in a number of ways, such as:

- Someone can run away with your money making false promises or stealing it.

- The counterparty can have a change of heart and dishonor a non-contractual agreement.

- The mechanism of exchange can stop functioning for any reason and is not guaranteed by the government.

- An unregulated instrument or asset class can be banned by the government.

In order to avoid this, a safe investment will have a mechanism of exchange (exchange, clearing house, regulator, etc.) as well as a legal contract (instrument) to facilitate it. These features are recognized by law and have a guarantee mechanism behind them.

For example, equity is traded and invested in by a government-recognized contract – stock or share. The shareholder of a company has rights that are guaranteed by the government including a legal recourse to salvage the assets in case of bankruptcy. There is a regulator, like SEBI in India, that defines and regulates the participants in equity markets right from companies who issue the shares, to exchanges, clearing houses, depository participants, and brokers.

An unsafe investment will lack either a proper mechanism of exchange and/ or a legal contract guaranteed by law.

Identifying unsafe becomes difficult when an investment option is quasi-legal. This means the government may recognize it as revenue but not recognize it as an investment (by providing regulation around it). This gives investors a false sense of safety that their money must be protected.

At the moment, digital assets face this situation in India. Profits on such investments are taxable, however, neither can the losses can be set off nor are there any regulations around such assets.

Finding Safety

The degree of safety of a particular investment is guided by what or who backs the instrument.

For example, government debt is safer than corporate debt. This is because government debt is backed by the tax generation capability and/ or assets of the sovereign in comparison to the revenues and/ or the assets of a corporation. The risk of default for government debt is much lower than for a corporation.

Even for a corporation, there are mechanisms in place to recover the principle and appreciation in case of trouble. These are set by the government and executed through regulators, courts, or tribunals. This makes it relatively safer in comparison to investments that are purely backed by trust.

A safe investment will be backed by a valuable asset and/ or a legal recourse to redress disagreements in value.

Decentralized investments run on the trust of the participants of a network. By their design decentralized investments, if not recognized by the government, are unsafe (they may or may not be risky). This is because their underlying trust can evaporate very quickly in troubled times and there is no mechanism to address the disagreement in value.

Risk Vs. Safety

Risk moves on a continuous scale. This scale can be linked to asset classes. Even within an asset class, there can be sub-categories that spell out the risk of the investment. This gives risk 2 dimensions to risk – (i) inter-asset risk and (ii) intra-asset risk. The diagram below gives an easy way of remembering the scale of inter-asset risk

The above scale is flexible with respect to the investor’s perspective.

On the other hand, Safety is binary. An investment is either safe or not safe. In order to assess safety, a simple checklist of criteria needs to be met.

- Is the asset recognized by law as an investment?

- Is the mechanism of exchange regulated?

- Is the instrument covered by a legal recourse in case of a dispute?

Risk & Safety

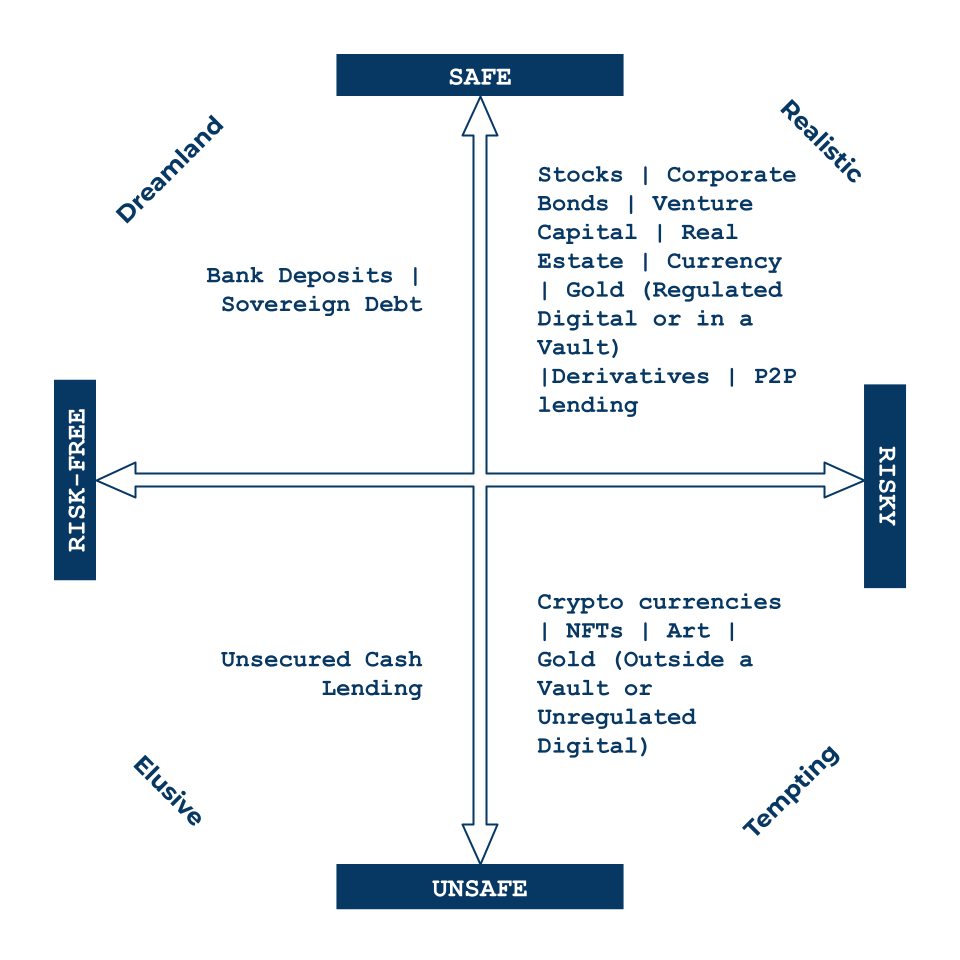

Investors can preserve their principle and yet make good returns if they are able to classify investments easily. At Modulor Capital we use the Risk-Safety Quadrant to easily classify investments into 4 buckets. On one axis we classify investments as Safe or Unsafe, while on the perpendicular axis, we classify an investment as Risky or Risk-free.

- Risky + Safe = Realistic

- Risky + Unsafe = Tempting

- Risk-free + Unsafe = Elusive

- Risk-free + Safe = Dreamland

Most investments are Realistic. They offer more and more returns for more and more risk but are regulated. This is where the reality (and also the tough challenge to produce better returns) lies. Regulated money managers need to work the hardest here.

The second category is Tempting. Here safety is compromised but the possible returns are very high. No matter how much experience an investor gains, such investments always tempt them to make a quick buck. Such investments are typically also popular with the younger generation since they feel closer to a new concept than to accept the tough route.

The third category is Elusive where an unsafe investment offers a smooth curve. Such an investment will also be offering a much higher return with a “sure-shot” return. These investments are good while they last.

The final category is the risk-free and safe category- Dreamland. Such investments preserve capital, give humble returns, and are the most boring ones. However, once in a while, such investments do offer good return prospects, especially in times of macroeconomic turmoil.

Classifying investments into 4 buckets simplifies the task of portfolio creation to identifying the amount of risk required and assigning weights to each type of investment to meet that requirement.

Risky isn’t Safe, and Safe isn’t Risk-free

As an investor, it pays to remember that Risk and safety are different things. Risk is associated with volatility and its resulting behavior while Safety is associated with regulation.

Looking to choose the right investment risks?

To invest with the appropriate amount of risk suitable to your profile into safe investments start a one-on-one Conversation here: https://modulorcapital.com/wealth-management/start-a-conversation-wealth-management/

About Us

Modulor Advisory Services is a Securities and Exchange Board of India (SEBI) Registered Investment Adviser (RIA) with license number INA100015115.