Quantamental Investment Objectives

Institutional investors fare better in all kinds of markets because they have a very clear set of investment directives. Alongside, seasoned investors employ very specific investment strategies with a highly disciplined and systematic approach. This gives them the edge over other investors in terms of returns generated and the risks they are exposed to.

Following directives and strategies help navigate the randomness of markets and achieve good investment outcomes. Directives and strategies are formed as a result of highly defined Investment Objectives. Something other investors lack the knowledge and understanding about.

Non-institutional and non-professional investors are not full-timers. It is simply beyond their expertise to be able to define investment objectives, forget alone have the discipline to follow them through.

Yet, investing is essential for any individual or family to preserve, accumulate or grow wealth in the long to medium term, along with shorter-term capital-appreciation, income-creation, and profit-generation.

Thus, there is a need to have a framework to define clear-cut investment objectives.

A Quantamental Solution to Investing like Institutions

Quantamental Investing® helps us to define investment objectives quickly and easily. Investment objectives can be both Quantitative (defined in terms of a returns distribution) and Fundamental (defined in terms of the underlying asset). This article will elucidate these objectives.

While fundamental investment objectives define who is the recipient of the investment and what instruments will be used to invest the money, the quantitative investment objectives are bothered with what the characteristics of the returns will be.

Both are essential to provide a logical and reasonable explanation as to why a strategy is being followed. This explanation forms the basis of making good investment decisions and also sticking to them.

These quantitative and fundamental investment objectives can be further overlapped to form simple Core and Satellite objectives usable by any ordinary investor. The following two articles would each describe these objectives. Let’s start with understanding Fundamental Investment Objectives.

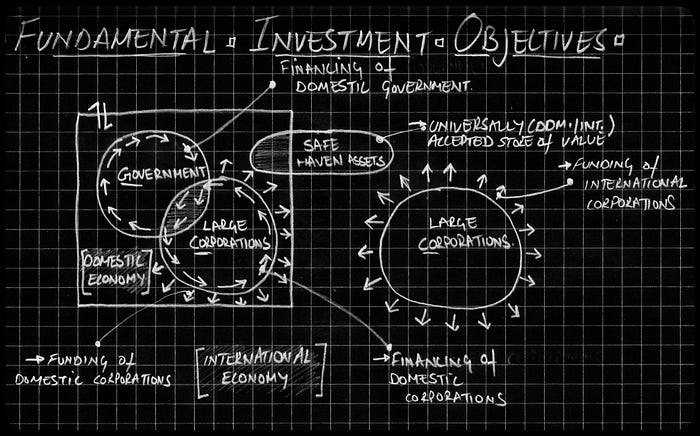

Fundamental Investment Objectives

From a fundamental point of view, investors can invest money in their own country (or the Domestic Economy) or another country (the International Economy). They also have a third option of investing in assets that are globally in demand (or Safe-haven Assets) like gold, commodities, currencies, etc.

Further, this investment can be made in 2 ways:

- Funding or giving the money to entities (like governments, corporations or individuals, etc.) in hope of growth of capital and earning dividends. An example is an equity stock.

- Financing or loaning the money to entities in return for a coupon or interest payment till the principal is returned. An example is holding debt.

Funding or financing are just different instruments that have different contractual behaviors. Funding instruments generally earn higher returns than financing instruments by forgoing the safety of collateral (that is provided by financing instruments). This means funding instruments (like equity) can go to nearly zero as well and are not backed by collateral as with financing instruments (like loans).

Corporations and individuals (or other similar entities) can raise money from both funding and financing, while governments typically only prefer financing (i.e. take loans to pay them back later through taxes) and may even fund corporations themselves. This is done at both the domestic and international levels.

The underlying asset to funding and financing that gives the growth of capital is human efforts. People work, create value, and consume value. This cycle makes the economies run.

The third type of asset is a store of value (in the short to long run). Gold is one such asset, which is recognized as a store of value by every economy and culture in the world. It acts as a hedge against the failure of an economic system.

Other commodities and currencies can also act as safe havens in which investors park at least some bit of their net worth to survive through tough economic times. These assets are driven by demand and supply mechanics.

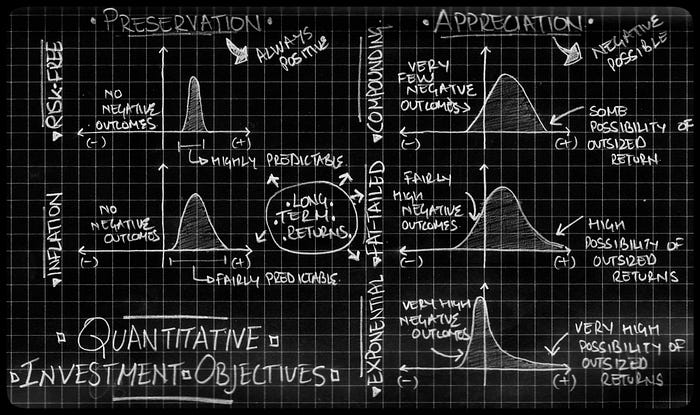

Quantitative Investment Objectives

Quants do not care how the returns are being generated, they are focussed on what the characteristics of these returns are. These characteristics are visually described in distributions (and many other numerical metrics which we will skip here to keep it simple).

The distribution of returns affects the experience of holding the investment. They have a direct impact on the psyche of the investor.

Volatile investments which pay well but go up and down may look attractive on the outside but often hurt the investor’s psyche with frequent swings in value. Stable investments, on the other hand, provide the comfort of easily holding them through long periods but often pay poorly than volatile investments.

By defining what the distribution of an investment would look like, investors can prepare themselves for the outcomes and the experience they will undergo while holding the investment to its maturity. This is one of the most important functions of defining quantitative investment objectives. It brings about the necessary behavioral control (for which the investors are rewarded).

While there are many types of return distributions, we identify 5 types that are well-suited to describe investment returns.

- Risk-free: A risk-free distribution as the name suggests is always positive (over the short, medium, and long run). It preserves value and is the most comfortable distribution to deal with. However, it pays the lowest return. Instruments such as Fixed Deposits or Overnight securities exhibit such a distribution.

- Inflation: The second distribution which preserves capital is inflation. This distribution may vary a bit in the short to medium term and give variable results. Inflation returns may seem negative in the short run (depending on the point of reference) but in the long run, always give positive returns. An asset class that displays inflation-linked returns over the long run is gold.

- Compounding: A compounding distribution is where serious returns that provide appreciation come into the picture. Occasionally, compounding returns may be negative, but the probability of this is low. Instruments like bonds show such return distributions.

- Fat-tailed: Stocks and other funding instruments show fat-tailed returns. This means there is a good probability that returns may be negative in the short run but are balanced by outsized positive returns once in a while (fat-tails). Fat-tail distributions need the investor to show emotional restraint (of not reacting to market moves) in the short run when returns can be negative. In the long run, fat-tail returns investments tend to show compounding-like return distributions. That is why holding broad-based index investments pay well in the long run.

- Exponential: The final and the most skewed distribution is exponential. Asset classes like Venture Capital exhibit such returns. This means most of the VC investments will give negative returns and only a handful will give positive returns. However, these positive returns will be so large that they will balance out the negative returns (over the long run and a large number of investments). Such investments need the most behavioral discipline and capital to realize the fruits of such a distribution. That is why VC investments have a typical holding period of 7+ years and require a large number of investments to be done by the investor.

Quantamental Objectives

Fundamental investment objectives give us an explanation as to why we should invest in a certain investment option. On the other, hand quantitative investment objectives describe the experience of holding the investment throughout its lifetime.

The two types of investment objectives can be combined to define any investment. However, we have found 6 combinations that hold more significance for investors than others. This is because certain themes carry more weight in the lives of individuals and families than others.

The first three of these combination objectives form the Core Investment Objectives described in the next article. The third article defines the Satellite Investment Objectives.